Ashraf Engineer

February 5, 2021

PODCAST TRANSCRIPT

Hello and welcome to All Indians Matter. I am Ashraf Engineer.

So much was expected from the Union Budget that Finance Minister Nirmala Sitharaman presented on February 1, 2021. India needs an economic recovery, employment and investment. Coming on the back of the crippling COVID-19 pandemic, India’s first ever technical recession and millions of job losses, the expectation was that Sitharaman would spend till it hurts and then spend some more. And she did. Only, it’s not as black and white as it would seem – what she didn’t tell you is perhaps more critical than what she did.

AUDIO CLIP

SIGNATURE TUNE

As she rose to present Union Budget 2021, Finance Minister Nirmala Sitharaman would have never felt more beleaguered. The economic distress across the country, which began even before the COVID-19 pandemic struck, is a mammoth challenge and her performance is under the microscope more than ever.

Over the past year, after many quarters of underperformance and then the pandemic, the Indian economy suffered its first ever technical recession. So, as Budget Day approached, the calls for more government spending, a comprehensive plan for banks’ non-performing assets and a healthcare revolution got louder. Sure enough, that’s what Sitharaman focused on.

The Budget detailed a massive economic boost through infrastructure expenditure, a 137% rise in healthcare spending and a high disinvestment target.

Infrastructure became the favoured route for government spending with massive outlays, especially in states where elections are coming up. There was also a Development Financial Institution with a corpus of Rs 20,000 crore to fund infrastructure and a tax-friendly system for foreign investment in infrastructure. The cash-strapped government also proposed to sell surplus land with ministries and public sector enterprises to fund infrastructure.

Healthcare got a booster shot with an outlay of Rs 2,23,846 crore, compared to Rs 94,452 crore in the current fiscal – that’s an increase, like I said, of 137%. This included Rs 35,000 crore for COVID-19 vaccines, more money for Prime Minister Narendra Modi’s pet project Swachh Bharat and an air pollution fund.

The government bit the bullet on the politically sensitive issue of foreign direct investment in insurance companies by raising the limit to 74% from the current 49%. As for banks’ non-performing assets, there will be a ‘bad bank’ that will take over the bad loans of public sector banks and clean up their books.

Sitharaman had clearly decided, to use her own words, to spend, spend, spend – and the fiscal deficit be damned.

This is what most experts were recommending, so that’s a good thing at this time, right? Wrong. The problem lies not in what the finance minister tells us but in what she isn’t saying. Let me explain.

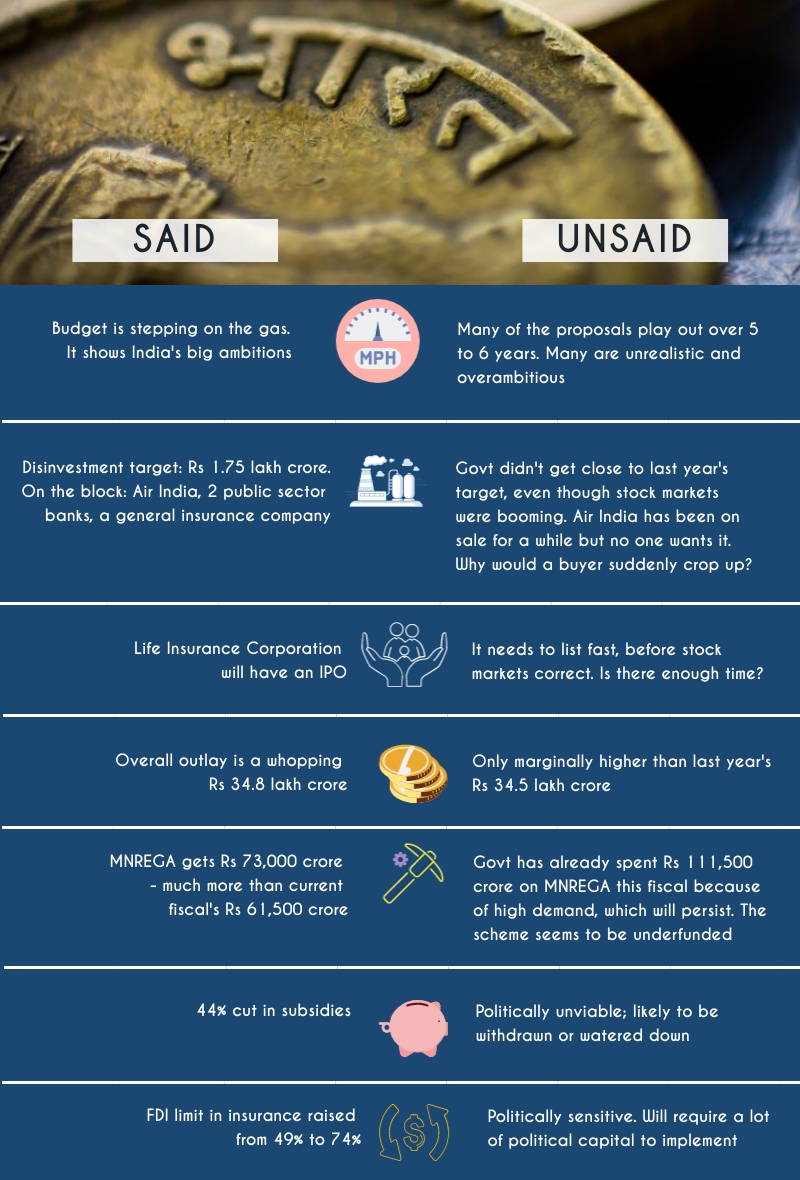

- The Budget seems like it’s stepping on the gas but many of the proposals actually play out over five or six years and the most talked about plans are in danger of never fructifying because they’re unrealistic, overambitious or poorly timed.

- Let’s take disinvestment first. This is critical for Sitharaman to find the money to fund the ambitious programmes she has announced. The target she has, Rs 1.75 lakh crore, includes the proceeds from the sale of Air India, a couple of public-sector banks and a general insurance company.

The problem is that the government didn’t even get remotely close to last year’s disinvestment target despite surging stock markets. Air India, in fact, has been on sale for a long, long time but nobody wants to touch it with a barge pole. What makes Sitharaman think that a buyer will magically materialise this year? The target seems overly optimistic.

- When in trouble, the government often leans on the Life Insurance Corporation to bail it out with its vast reserves of funds. So, this year, the government will do it again – only this time, it is using an IPO for LIC. But it’s a time consuming process and it needs to happen before there is a correction in the stock markets. The government may not have as much time as it needs.

- As I indicated earlier, what the finance minister didn’t tell you was perhaps more important than what she did say. For example, she had much to say about the overall expenditure of Rs 34.8 lakh crore – it’s a gargantuan number. Only, it’s just a marginal rise over the Rs 34.5 lakh crore budgeted last year.

- Let’s look at the Mahatma Gandhi National Rural Employment Guarantee Act programme, better known as MNREGA. It is a critical social security net that guarantees poor families employment over a certain number of days every year. It is the sole reason millions of families, especially in rural India, are able to keep their heads above the water.

This year, Sitharaman budgeted Rs 73,000 crore for it – way higher than the Rs 61,500 crore it got last year. What she doesn’t say is that it is significantly lower than the Rs 111,500 crore actually spent on MNREGA in 2020-21. This was because the widespread job losses led to a sharp rise in MNREGA demand – which has persisted up to the presentation of the Budget and is likely to continue for a long time.

India has virtually phased out the lockdown but it will be a while before employment generation picks up pace. Until then, MNREGA demand will remain higher than usual and Sitharaman will almost certainly have to spend more than she’s allocated for it.

- Now let’s consider something else that’s tough to pull off – subsidy cuts. In order to find the money to fund all the proposals, Sitharaman has had to squeeze expenses – that’s understandable and required. The Budget has proposed a 44% cut in subsidies – that’s politically unviable and seems a hope more than anything else.

- FDI in insurance is another politically sensitive issue and no matter who takes over banks’ bad loans, someone will have to pay.

It’s likely that some or many of the more difficult decisions – such as subsidy cutbacks – will be withdrawn or watered down, thus reducing the impact of the Budget.

In fact, the more you look at it, the more the Budget reminds you of the so-called fiscal stimulus last year. The stimulus was touted to be 10% of the GDP. It turned out that a large component of it comprised steps taken earlier or assigned to agencies outside of the government. Experts later estimated the stimulus to be a mere 1% of the GDP – a tenth of what was claimed by the Modi government.

What Sitharaman’s handed us is a very attractively wrapped package. But what will we be left holding when the wrapping comes off?

Thank you all for listening. Please visit www.allindiansmatter.in for more columns and audio podcasts. You can follow me on Twitter at @AshrafEngineer and @AllIndiansCount. Search for the All Indians Matter page on Facebook. On Instagram, the handle is @AllIndiansMatter. Mail me at editor@www.allindiansmatter.in. Catch you again soon.