Ashraf Engineer

January 1, 2022

EPISODE TRANSCRIPT

Hello and welcome to All Indians Matter. Happy new year. I am Ashraf Engineer.

In recent years, there has been great emphasis by governments – both UPA and NDA – on financial inclusion. A critical first step has been starting bank accounts for those without access to banking services. This is often referred to as ‘banking the unbanked’. However, India has achieved only limited success on this front. Even today, many choose costly, risky options such as borrowing from moneylenders or hiding currency in a mattress. India has roughly 190 million unbanked adults and, according to the World Bank, this is second only to China among developing countries in the number of citizens who don’t have bank accounts or participate in the formal financial sector. Millions of basic accounts were opened under a policy mandate, which covered at least 80% of Indian adults. However, half of these are estimated to be inactive. At least part of the reason is the unspoken cost of starting and opening bank accounts for the very poor.

SIGNATURE TUNE

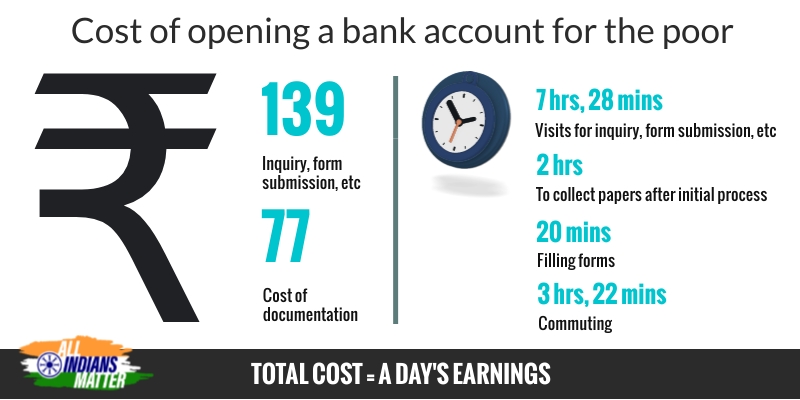

Did you know that opening a bank account can cost you? According to a Reserve Bank of India report, if you visit a bank thrice to open an account — for inquiry, form submission, etc— it would cost Rs 139. The time you would spend doing this would be an incredible 7 hours and 28 minutes. Add to these other burdens, such as dealing with unhelpful bank staff and documentation issues, and the exercise gets even more complex.

Referring to an audit carried out in 2016, the report says it takes two hours to collect papers after initial procedures and the cost of documentation adds up to Rs 77. Roughly 20 minutes go in filling forms and the time spent travelling is 3 hours and 22 minutes. The report goes on to say that the total cost of this transaction for the poor is equivalent to a day’s earnings.

This is money and time the poor simply don’t have.

No wonder the push to draw millions into the banking fold isn’t working as well as hoped. Financial inclusion is vital if we are to progress as a nation but the transaction costs are proving to be a serious hurdle.

The RBI report says technology could be the answer. Once the Jan Dhan programme for financial inclusion, Aadhaar registration and mobile phones percolate to the bottom of the pyramid, banking costs could reduce drastically. However, this is hypothetical and the situation as of now isn’t encouraging.

Also, let’s look at banking inclusion for what it really is. It’s not just about having access to certain financial services; it’s much bigger than that. It’s about democracy and equality.

The world over, financial inclusion is being looked at as the new measure of economic growth that can seriously dent poverty levels. It is critical to reducing the gap between the rich and the poor and is about delivery of services to the disadvantaged at affordable terms. Therefore, it has as much to do with social progress as financial.

India comprises 1.3 billion people spread across 28 states and eight union territories. There are 6.6 lakh villages and 748 districts. An ocean of people in the rural areas are excluded from access to banks because, as of 2019, only 33% of public sector bank branches were in these locations.

The RBI has been pushing banks to extend their networks to villages through branches and ATMs but it’s slow going because many banks find it a loss-making proposition. They point out that they have a duty towards their own clients and shareholders to maintain healthy balance sheets.

Let’s look at some of the other factors affecting banking inclusion.

First, location. Most banks operate in commercial areas and the branches are located such that they are profitable. Most banks find rural locations to be unprofitable, cutting out a large section of the population. For this population to access banking services, it has to travel large distances. So, banking becomes as much about transportation infrastructure as the services it provides.

Second, absence of documents. Many Indians don’t have birth certificates or other proof of identity or address. Banks tend to turn them away. There is also gender bias – women tend to have little property in their name and so they are denied loans. Often, they are asked to get male guarantors before credit is provided.

Third, little understanding of banking services. India performs abysmally on financial literacy. Millions don’t know what financial products are available or how to use them.

Fourth, the fine print. Financial products and services come with certain conditions – for instance, minimum balance requirements for accounts. If the balance is not maintained, there are penalties and so the poor feel they are better off without the account.

Fifth, occupation or type of business. Most banks shun small borrowers and unorganised enterprises when it comes to providing loans. Rejected, these borrowers have no choice but to turn to local moneylenders or extended families.

We’ve seen this exclusion manifest itself in various ways. One example of this is the alarming number of farmer suicides over the past few years. While that is a complex issue spanning procurement and distribution at one end to climate change on the other, part of the reason is lack of institutionalised credit.

Scrambling to meet its financial inclusion agenda, the Centre sent banks – both public-sector and private – a list of locations where branches should be opened in the current financial year. At the time it was said that the Centre had asked for at least 15,000 new branches, presumably in rural areas. The Finance Ministry mandate was to open a branch within 15 km of any village where there were no banking facilities available. We won’t know how successful this directive was until after the financial year ends and there is an audit. But, I hope for the best. Because, without it, it’s not just our economic problems that would get worse, but also our social divisions.

Once again, I wish you a joyful and prosperous new year.

Thank you all for listening. Please visit allindiansmatter.in for more columns and audio podcasts. You can follow me on Twitter at @AshrafEngineer and @AllIndiansCount. Search for the All Indians Matter page on Facebook. On Instagram, the handle is @AllIndiansMatter. Email me at editor@www.allindiansmatter.in. Catch you again soon.