Ashraf Engineer

June 28, 2025

EPISODE TRANSCRIPT

Hello and welcome to All Indians Matter. I am Ashraf Engineer.

Sovereign debt levels of developing economies are impacting macroeconomic stability, warn economists. At least 50 developing countries spend more than 10% of their revenues on debt servicing, according to a UN Trade and Development, or UNCTAD, report in late 2024. This is squeezing government finances and creating risks.

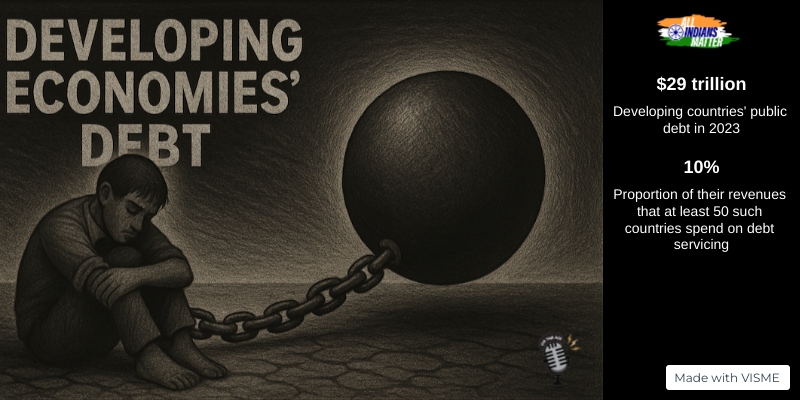

To be clear, public debt can be vital for development. Governments use it for infrastructure, social welfare programmes and for other expenditure to improve living standards. However, if it grows too much or too quickly, it is a massive burden. Unfortunately, this is what is happening in the developing world. The UNCTAD report says that global public debt hit a record high of $97 trillion in 2023, with developing countries accounting for $29 trillion. Their debt has grown twice as fast as the others’ since 2010. This means that developing countries’ interest payments are growing so fast, they are outpacing critical public expenditure on services such as health and education. For example, during the initial part of the COVID-19 pandemic, Africa, Asia and Oceania (excluding China) spent more on interest payments than on health.

More than 3.3 billion people live in developing countries that spend more on interest payments than on critical services. In these countries, interest payments also outweigh climate investments, adding further risks to existing vulnerabilities.

SIGNATURE TUNE

Make no mistake, your country’s high debt levels have a direct impact on you. For example, it could lead to shortages and high inflation, thus impacting stability. Last year in Kenya, violent clashes erupted after the government tried to raise taxes to mitigate a debt crisis. Interest payments had burgeoned to 60% of government revenues.

It’s no surprise that the World Economic Forum’s latest edition of the Chief Economists Outlook report said most chief economists believed that high public debt is a threat to macroeconomic stability in both advanced and developing economies. Almost 40% of the chief economists surveyed expected defaults to rise in developing economies in 2025. The debt will undermine government efforts to push growth and leave nations ill-prepared for any economic downturn that may occur. Developing countries especially will struggle with challenges such as energy transition, demographic shifts and national security.

So, what is India’s external debt? It increased by 10.7% to $717.9 billion at the end of December 2024 from $648.7 billion in December 2023, as per Finance Ministry data. India is fortunately servicing manageable levels of debt and is showing far more fiscal discipline than many other developing countries. However, a global debt crisis triggered by other countries’ defaults will not leave India untouched.

Asia and Oceania hold 27% of global public debt, followed by Latin America and the Caribbean at 5% and Africa at 2%. The interest burden varies significantly, with countries’ ability to repay worsened by inequality embedded in the international financial architecture. For developing countries, servicing of external debt reached $365 billion in 2022, which was equal to 6.3% of their export revenues. For perspective, the 1953 London Agreement on Germany’s war debt limited the amount of export revenues that could be spent on external debt servicing to 5%.

Today’s debt dynamic is largely a result of higher borrowing costs imposed on the developing countries. Developing regions borrow at rates that are two to four times higher than those of the US and six to 12 times higher than those of Germany. Borrowers cite a greater risk of default to justify the higher rates.

To add to that, developing countries experienced a net resource outflow when they could least afford it. In 2022, they paid $49 billion more to external creditors than they received in disbursements. Who pays the price? Regular people who can least afford to.

There has been a rise in interest rates across the world since 2022 because of soaring inflation and this has impacted public budgets. So, developing countries’ interest payments on public debt hit $847 billion in 2023, a 26% rise from 2021. In 2023, 54 developing countries allocated 10% or more of government revenues to interest payments.

Let’s take a look now at how this crisis evolved.

Its origins can be traced to the oil-price shock of 1973-74. The Organization of the Petroleum Exporting Countries, or OPEC, limited supply of oil, leading to a sharp spike in prices. That hurt all importers of oil, including many newly independent African countries. OPEC’s excess profits were invested in the Western commercial banking sector and so the banks needed new borrowers to lend that money to. Developing countries, which were struggling because of the oil shock, needed development assistance. These then became the recipients of debt from the western commercial banks. This flow of funds from OPEC to commercial banks and from there to developing countries was called ‘petrodollar recycling’.

This rising external debt first came into the spotlight in the early 1980s. There were three key factors for this. First, a second oil-price shock in 1979 that led to a recession in the West and further strained the balance of payments of oil-importing developing countries. The same commercial banks then offered further loans to tide the developing countries through. Second, there was a shift in policy in the West to use interest rates to control inflation. As inflation rose because of the rise in oil prices, interest rates also rose to contain it. This further increased the costs of debt servicing for developing countries. Third, the recession in the West shrank developing countries’ export markets, making it even more difficult to meet interest payments.

As I said earlier, while debt itself is not new or unique to the developing world, it’s a problem when nations can’t meet the repayments. Many nations have defaulted down the decades. For example, in August 1982, Mexico said it could no longer meet repayments on external debt. In the years that followed, many poor countries had to institute crippling austerity measures so that they could service their debt.

In 2010, the total external debt of all developing countries was $4 trillion, which represented 21% of their gross national income, according to a World Bank study.

You could look at this in a couple of ways. The West, for instance, views it as a threat to the stability of the international financial system. As an extension of that, it feels that the responsibility for the crisis rests with the borrowing countries. This view ignores how the crisis unfolded in the first place as well as the underlying problems of the developing economies.

Another view, this one proposed by the developing world, argues that the debt is an imperative of development. These countries have been left behind often by the actions of the West itself, such as colonisation. Therefore, it is argued, that a lot of the responsibility rests with the West as well as the commercial banks that lent the money through a reckless strategy.

Initially, the response to the crisis focused on short-term measures to prevent defaults. The IMF and the World Bank offered loans with conditions such as structural adjustments of the economies designed to increase their productivity.

By the mid-1990s, however, it was clear that a long-term approach was needed. This was because, despite developing countries accepting IMF and World Bank conditions, the debt crisis persisted. Some measures, such as limited debt relief, were taken. However, the crisis has persisted still and now many have called for wholesale debt cancellation.

The argument is that poorer countries should not be forced to choose between servicing debt and serving citizens. Policymakers are contemplating various relief mechanisms. For example, Spain called on creditors to incorporate the so-called pause clause that allows developing countries to suspend debt payments during a disaster. Grenada became the first country to use it, suspending bond payments after a hurricane hit in July 2024.

So, what are the options for developing economies’ governments?

One could be restructuring the debt before it reaches unsustainable levels. Such economies are vulnerable to high interest rates, which would further raise their borrowing costs. With already weak economies, a natural disaster or one bad decision could mean the debt becomes unsustainable. This would increase hardships for the poor. Sri Lanka is one such example. Its debt was considered unsustainable in 2020 but it reached out to the IMF for restructuring only in 2022 – after its reserves had fallen to less than $20 million.

The other option before governments is to increase progressive tax collection. This is a system in which the tax rate increases as an individual’s income rises. It follows the principle of higher-income earners paying a larger percentage of their earnings in taxes compared to lower-income individuals. Progressive taxes are preferred because they reduce inequality. Indirect taxation, on the other hand, affects the poor. Indirect taxation includes value added tax, customs duties and service tax. In such a system, the poor and rich may consume roughly the same quantity and therefore pay the same amount of taxes.

A third option could be to increase government efficiency. Inefficient government spending and wastage are serious burdens on citizens. Such countries also tend to have a larger public sector, which adds to the fiscal burden that is offset by higher taxes and debt. So, rationalising the size of the government is critical. In Africa, inefficiency in public spending leads to a loss of more than 2.5% of GDP annually. Transparency and digitisation of systems can reduce wastage and corruption. However, such moves do face great institutional resistance.

IMF research shows that improving governance in Africa can reduce inefficiency in government spending and recover up to 50% of their returns on investment in infrastructure.

Lastly, governments should aim for greater economic growth. To do that, they need to attract large-scale foreign investment and increase ease of doing business. They also need trade liberalisation as well as investments in education, health and infrastructure. If growth is inclusive, it will increase foreign exchange earnings and shrink external debt.

A word about the onus on wealthier economies. They have a duty to not look away because billions live in low and lower-middle income countries. If they are hit by an economic contagion, the malaise will spread. The World Bank’s International Development Association has been a lifeline for the poorest economies in recent years and it needs more support. Also needed are multilateral efforts to speed up debt restructuring.

What’s clear is that urgent steps are needed to reduce developing countries’ external debt. Without that, global economic stability would be under a cloud.

Thank you all for listening. Please visit allindiansmatter.in for more columns and audio podcasts. You can follow me on Twitter at @AshrafEngineer and @AllIndiansCount. Search for the All Indians Matter page on Facebook. On Instagram, the handle is @AllIndiansMatter. Email me at editor@allindiansmatter.in. Catch you again soon.